O' Bubble, Where Art Thou?

A prequel to "The AI Cost Problem Nobody Has Priced In"

Three years ago, when OpenAI released ChatGPT to the general public, it sparked a wave of excitement unlike anything the technology industry had seen in decades. Researchers had long predicted that advances in Artificial Intelligence and Machine Learning would fundamentally reshape how we live and work. Suddenly, those predictions felt tangible.

The conversational nature of ChatGPT made it easy to interact with, and the enormous amount of data it had already digested by then (including much of the open web as well as thousands of books and other sources of knowledge) made it genuinely useful across a broad range of tasks. For many people, this was their first direct experience with technology that appeared capable of reasoning, creating, and solving problems at a level previously reserved for humans.

The age of Large Language Models (LLMs) had arrived.

As with any new potentially transformative technology, investors, entrepreneurs, and corporate leaders quickly began searching for ways to participate in the opportunity. The LLMs themselves became the immediate focus of attention, with capital pouring into OpenAI as well as a rising set of competitors, including Anthropic.

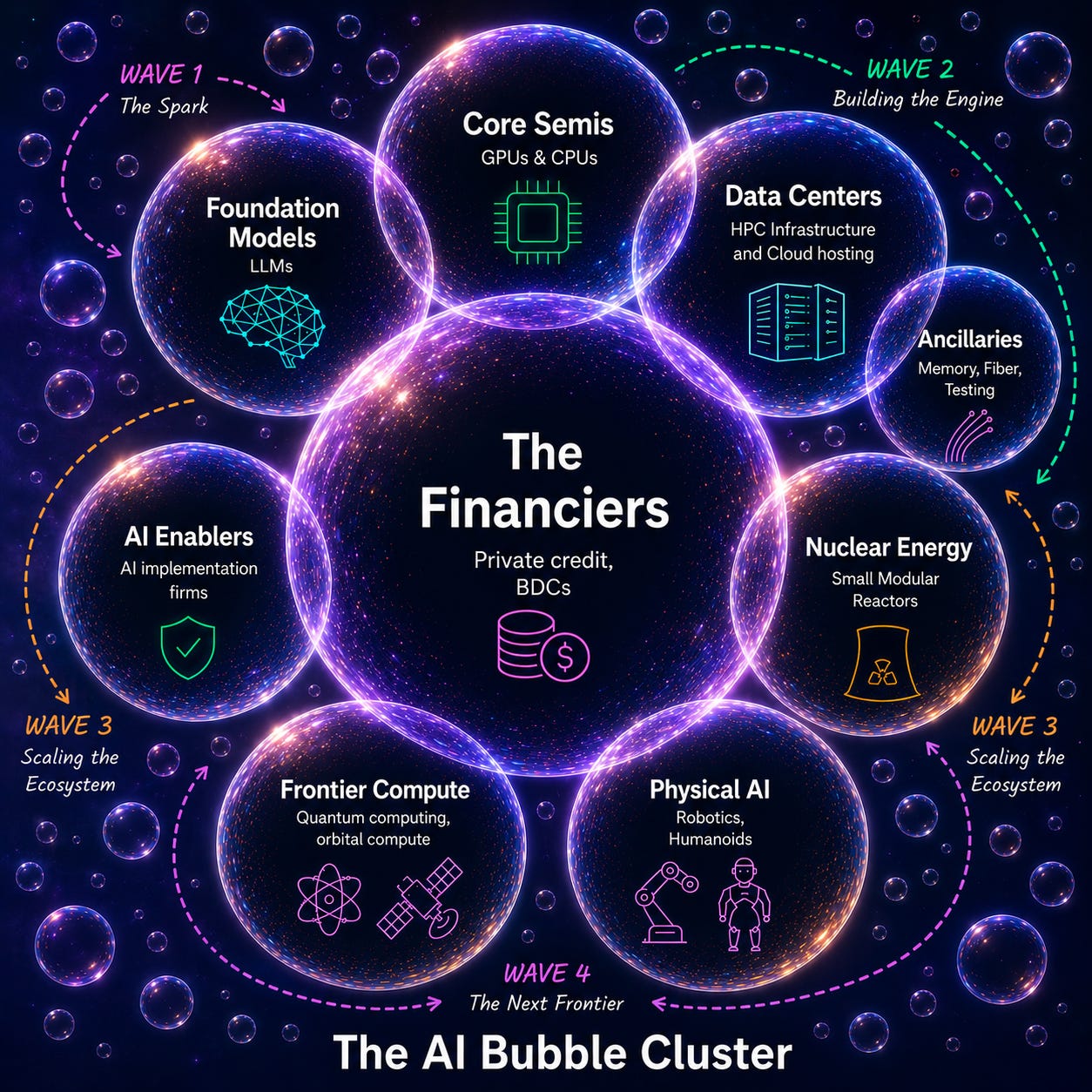

That turned out to be the first visible bubble: AI models & the companies building them.

The underlying models improved rapidly - capabilities that initially appeared novel soon demonstrated practical applications in software development, customer support, content creation, research, and knowledge-intensive professional services. Corporate customers searching for productivity growth in a slowing economy embraced the technology with both hands.

The second bubble followed almost immediately: Semiconductors.

Suddenly demand rocketed for the specialized GPU semiconductor chips that were needed to train and power these models. Capacity became constrained as hyperscale cloud providers, software platforms, and technology companies raced to secure supply and inventory literally had to be allocated, usually never fully up to the customer’s original order quantity. Revenues for these semiconductor companies went through the roof.

Large software and cloud companies that had established a near-stranglehold on their respective domains saw this technology as a potential existential threat. Some partnered with LLM developers to incorporate these models into their software and simultaneously went on a buying spree to secure as much GPU capacity as they could, so they could deploy them into their cloud infrastructure. With increasing end-user adoption though, cloud capacity itself became an emerging limitation.

Data centers quickly became the next logical point of investment in the supply chain. Hosting the compute required to serve all of the AI demand required the construction of large swaths of data-center capacity, with all its attendant needs from land to wiring to installation and service technicians. Of course, data centers needed a lot more power to run them, especially since the early generation of chips weren’t particularly efficient.

Thus emerged the third bubble: infrastructure, driving a huge part of the growth in the traditional economy.

It also turned out that speeding up responses required specialized memory and optical fiber—lots of it.

That led to a whole new set of second-order booms.

Just like the chip makers, the companies making memory, fiber for networking and other associated components also started selling out production several quarters in advance and literally had to keep customers at bay as everyone jostled to get ahead in this gold rush.

Any reluctance that boards of these highly manufacturing-intensive companies had about jumping aboard the AI train disappeared when they saw quarter after quarter of rising demand. To take advantage of the continuing growth, every company in the supply chain made the investments required to expand production capacity, confident that whatever they produced would be absorbed by a demand curve that seemed to have no ceiling.

AI was being adopted across an increasing swath of industries—not just in software coding but also customer service and accounting to legal research and countless other knowledge-based functions.

Naturally, consulting and AI implementation firms were experiencing a boom of their own, as they were being tapped by every company to help with the rollout.

Essentially any repetitive task powered by a body of knowledge appeared ripe for automation, provided appropriate guardrails could be established. Even content generation and creative fields such as art and music were not left behind. AI suddenly enabled many people who had previously lacked either the time or the skillset to participate, dramatically increasing accessibility while reducing cycle times.

That’s when things started to get really interesting.

Companies started to explore how to de-bottleneck the scaling of AI, leading to third-order effects in industries far removed from the direct AI supply chain.

As demand for power rose sharply, capital began flowing toward what many viewed as the most exciting source of future energy: nuclear power, particularly Small Modular Reactors (SMRs). Long viewed as politically difficult following Three Mile Island, nuclear energy was suddenly back in favor, but in a modified and compact form.

Investors started to look at quantum computing as the next frontier in computational capability, with the possibility of solving classes of problems that remain difficult or impractical for even today’s most advanced systems.

AI-powered humanoid robots and robotaxis became symbols of the future of work.

Meanwhile, pushback from communities to all of this new infrastructure popping up in their neighborhoods was equally palpable. Few people wanted a data center across the street generating noise, consuming enormous amounts of electricity, straining local grids and tapping into limited local water supply for cooling.

Given the constraints around power, land and local opposition, some investors began exploring ideas that would have sounded far-fetched only a few years earlier—orbital data centers began moving from science fiction to serious discussion.

Before you knew it, bubbles seemed to be popping up wherever one looked, all predicated on the same glorious future of AI that appeared to be just around the corner.

At this point, it is worth pausing to make an observation.

These are not really independent bubbles.

The economics of data centers and chip manufacturing depend on continued growth in AI demand. The economics of new power generation depend on continued growth in data-center capacity. The case for robotics depends on continued advances in AI. Quantum computing is often justified by future computational requirements that have yet to materialize. Many of these sectors are effectively underwriting one another’s growth assumptions.

Rather than existing separately, they resemble a cluster of partially fused bubbles, each drawing support from expectations embedded in the others.

None of these bubbles would have been possible without one important ingredient: capital

Which raises an obvious question.

Where is all the funding coming from?

The answer is probably closer to home than most investors realize.

Just six years ago, the Fed unleashed trillions of dollars through quantitative easing and adopted near-zero interest rates as the economy threatened to buckle under the weight of Covid. While these actions were critical in preventing a depression and stopping global financial markets from seizing up, it was never going to be easy to calibrate an intervention of that magnitude perfectly.

When Covid receded, the consequences became increasingly visible. Inflation surged to levels not seen in decades, asset prices rose sharply, and perhaps nowhere was this more evident to the layman, than in housing.

After the Global Financial Crisis of 2008, regulators and lawmakers had worked furiously under public pressure to limit the risks that banks could take while increasing capital requirements to strengthen the financial system. The result was that many forms of risk-taking gradually migrated outside traditional banking channels to a relatively nascent sector of private credit, which was originally funded by well-heeled investors who were looking for high returns but also had the cushion to take the hit, if the investment went south.

Private credit funds effectively provide a mechanism through which investors can access higher-yielding loans and financing opportunities that are often unavailable in public markets. The associated sector of Business Development Companies (BDCs), originally created to provide financing to small and medium-sized businesses. Unlike public markets, investments in private credit are not traded daily and therefore do not have a process for continuous price discovery. Their underlying values can appear more stable than equivalent publicly traded assets, even when the economics beneath them may be changing.

Over time though, a sizeable portion of the excess liquidity generated by the Fed found its way into private markets, reaching for higher yield (and potentially ignoring the higher risk).

Pension funds, insurance companies, family offices, endowments, and yes, banks themselves, have all participated in this migration of capital.

Which gives us the final bubble (and perhaps the least visible one of all): The funding bubble.

The assumption embedded in much of this ecosystem is that capital can continue generating superior returns from investments tied, directly or indirectly, to the same growth narratives driving the broader AI boom. Not every part of the market participated equally in this enthusiasm. Many mature, dividend-paying businesses generating significant cash flow were largely ignored as capital gravitated toward narratives promising transformational growth.

And as I discussed in my previous article, the one question all of these bubble-makers forgot to take into account is:

What happens when the conversation shifts from possibility to economics?

Because while markets can ignore costs for a surprisingly long time, businesses eventually cannot.

This publication examines technology, business, and capital markets through the lens of operating economics and the often-overlooked twin realities of execution and incentives.

The AI profit margins are negative or slim at the moment, unless you are providing the chips and infrastructure.

And even if OpenAI, Grok, and Anthropic decide to act as a cartel and all raise token prices together ... China 🇨🇳 is still providing good AI models which are cheaper.